FEATURE

Accelerating Collaborative Sustainability in the Tapes Industry

Trends and Opportunities in Pressure-Sensitive Adhesives: Sustainability, Innovation, and Market Growth

Opportunities to increase market share will increase when companies are pre-positioned for growth in a resilient and scalable way.

Trends and Opportunities in Pressure-Sensitive Adhesives: Sustainability, Innovation, and Market Growth

By Lisa Anderson, Founder and President, LMA Consulting Group

By Chirag Tripathi, Associate Director, MarketsandMarkets, Pune, India, and Parag Shah, Manager, MarketsandMarkets, Pune, India

Acrylic and water-based technologies dominate due to performance, versatility, and regulatory compliance.

Pressure-sensitive adhesives (PSAs) are a distinct class of adhesives that form an instant bond with substrates upon the application of light pressure, eliminating the need for heat, water, or solvent activation. Typically formulated from polymers such as acrylics, rubber, silicones, and polyurethanes, PSAs offer a well-balanced combination of tack, peel adhesion, and shear strength. This unique performance profile enables efficient bonding across a wide range of surfaces, making them highly versatile for applications in tapes and labels, packaging, hygiene products, medical devices, automotive components, and electronics.

The PSA market is experiencing growth due to several key factors. These factors include growing demand from packaging and labeling applications, growing shift toward sustainable and low-VOC adhesive technologies, rising adoption in hygiene and medical applications, and expansion of the e-commerce and logistics sector. These factors are reinforcing the strong growth trajectory of PSAs, positioning them as a critical enabler of efficient, sustainable, and high-performance bonding solutions across a diverse range of end-use industries.

The market for PSAs is projected to grow from $14.22 billion in 2025 to $16.53 billion by 2030, at a compound annual growth rate (CAGR) of 3.0%, between 2025 to 2030.

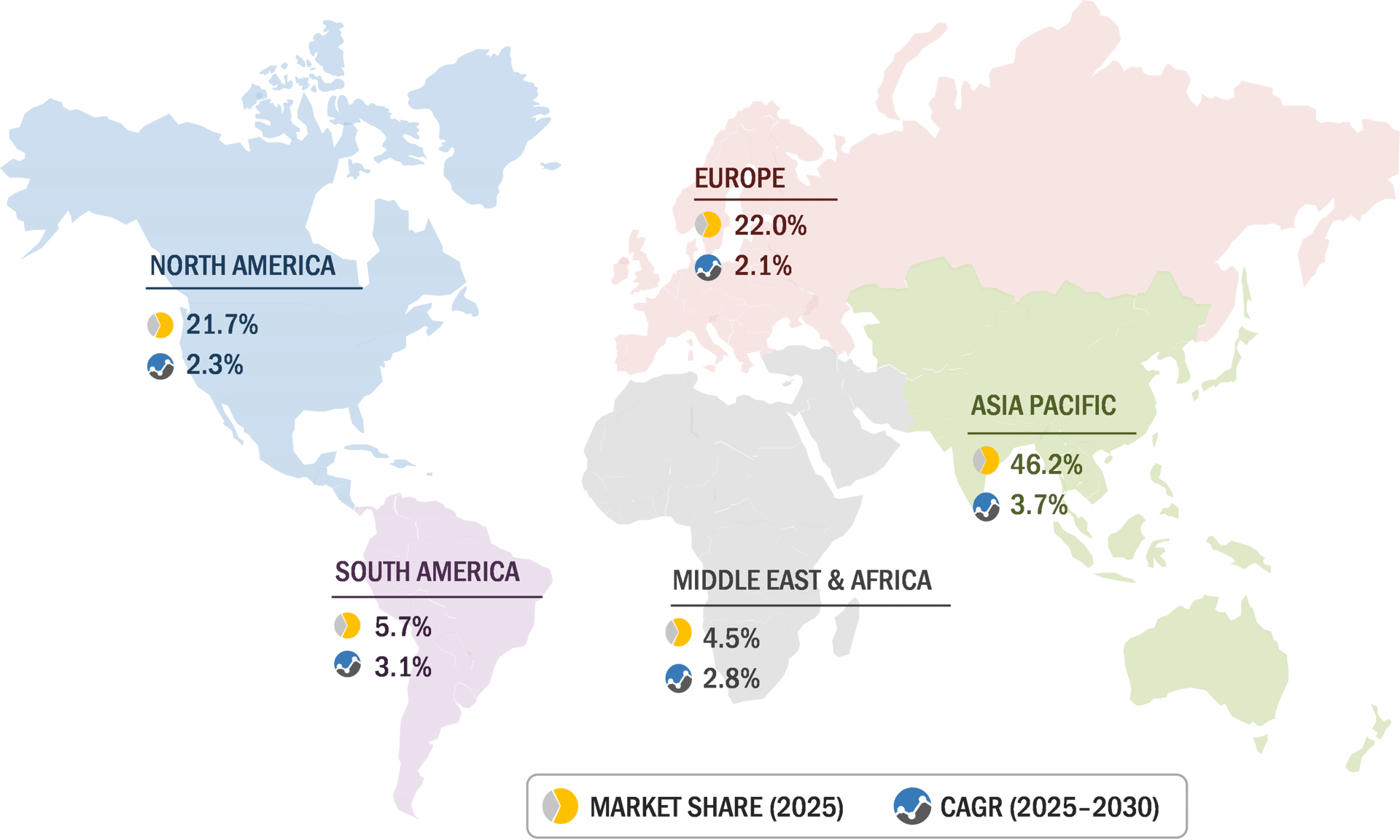

Figure 1: Asia-Pacific led the global PSA market in 2025. Source: secondary research, interviews with experts, and MarketsandMarkets analysis.

Asia-Pacific: Steering the Future of PSAs

Asia-Pacific has emerged as the dominant region in the market for PSAs, underpinned by a strong convergence of demand-side momentum, manufacturing capabilities, and evolving technological adoption. The region's growth leadership is primarily driven by robust expansion in end-use industries such as packaging, electronics, automotive, and hygiene products, supported by rapid urbanization, rising disposable incomes, and the continued expansion of e-commerce. Countries such as China, India, Japan, and South Korea serve as major consumption hubs, with large-scale production of tapes, labels, and flexible packaging materials further amplifying PSA demand.

On the supply side, Asia-Pacific benefits from a well-established manufacturing ecosystem, cost-competitive production, and easy access to raw materials, attracting both global adhesive manufacturers and regional players working to expand their footprint in the region. In parallel, increasing regulatory awareness and sustainability commitments are accelerating the shift toward water-based, hot-melt, and other low-VOC PSA technologies, particularly in developed markets such as Japan and South Korea. Additionally, the region is witnessing growing investments in high-performance and specialty PSAs tailored for advanced applications in electronics assembly, electric vehicles, and medical devices. This combination of strong end-use demand, manufacturing scale, and progressive technological transition firmly positions Asia-Pacific as the epicenter of growth and innovation in the global PSA market.

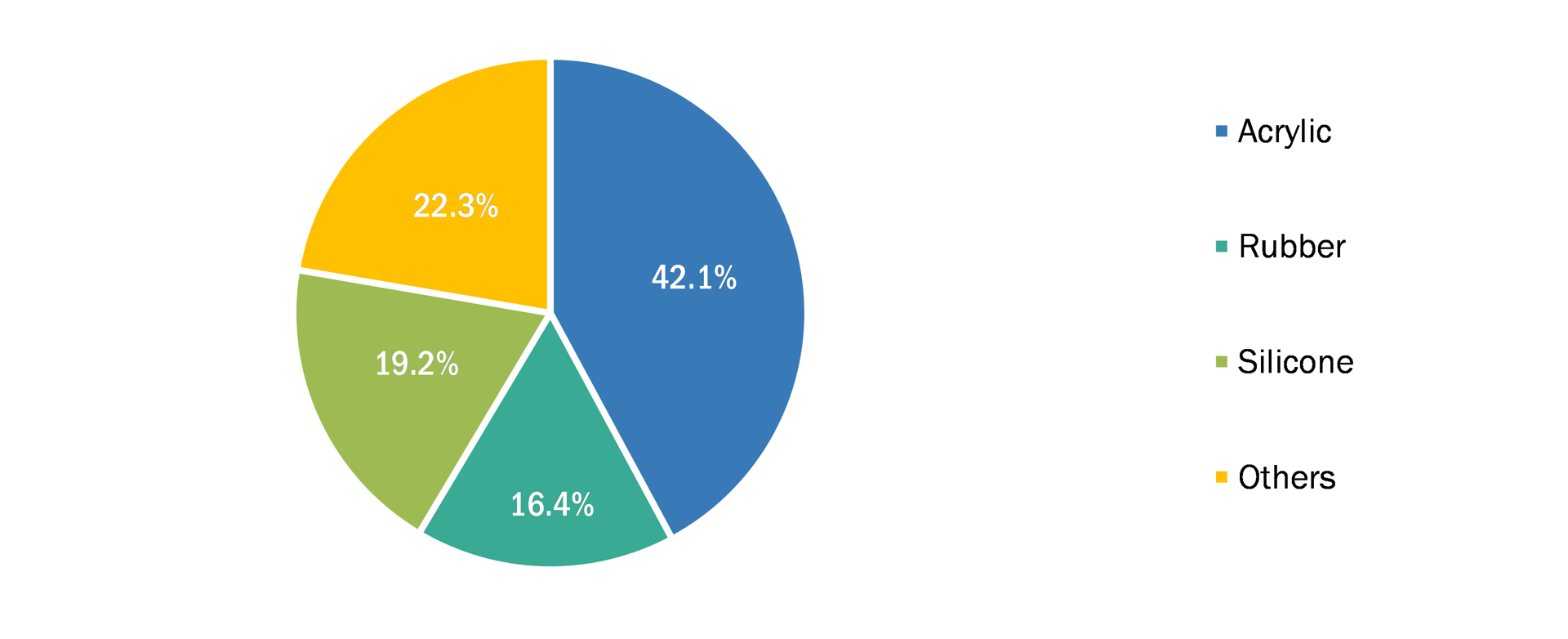

Figure 2: Acrylic was the largest chemistry in the PSA market in 2025. Note: Other chemistries include EVA, polyurethane, hybrid, and hydrophilic. Source: secondary research, interviews with experts, and MarketsandMarkets analysis.

Acrylic: The Backbone of PSAs

Acrylic-based PSAs dominate the market, largely due to their strong alignment with high-volume, performance-sensitive applications across packaging, labelling, and industrial tapes. In packaging and labelling, acrylics are preferred for their ability to deliver long-term adhesion, clarity, and resistance to environmental factors such as UV exposure and oxidation — critical for product labelling, branding, and outdoor durability. In automotive and construction applications, acrylic PSAs are increasingly used in bonding trims, emblems, and protective films, where durability and aging resistance are essential. Furthermore, their compatibility with water-based and UV-curable technologies makes them the chemistry of choice in regions with stringent environmental regulations, reinforcing their dominance in both mature and emerging markets.

In contrast, silicone-based PSAs occupy a strategically critical position, driven by their indispensable role in specialized, high-performance applications. Their adoption is particularly prominent in electronics, where they are used in insulating tapes, thermal management materials, and component assembly requiring stability under elevated temperatures. In the medical sector, silicone PSAs are favored for advanced wound care and wearable devices, where skin compatibility and performance under varying physiological conditions are key. Additionally, their ability to bond low-surface-energy substrates makes them essential in niche industrial and aerospace applications. While their higher cost restricts their penetration in mass-market segments, silicone PSAs continue to gain traction in value-driven applications, where reliability under extreme conditions outweighs cost considerations.

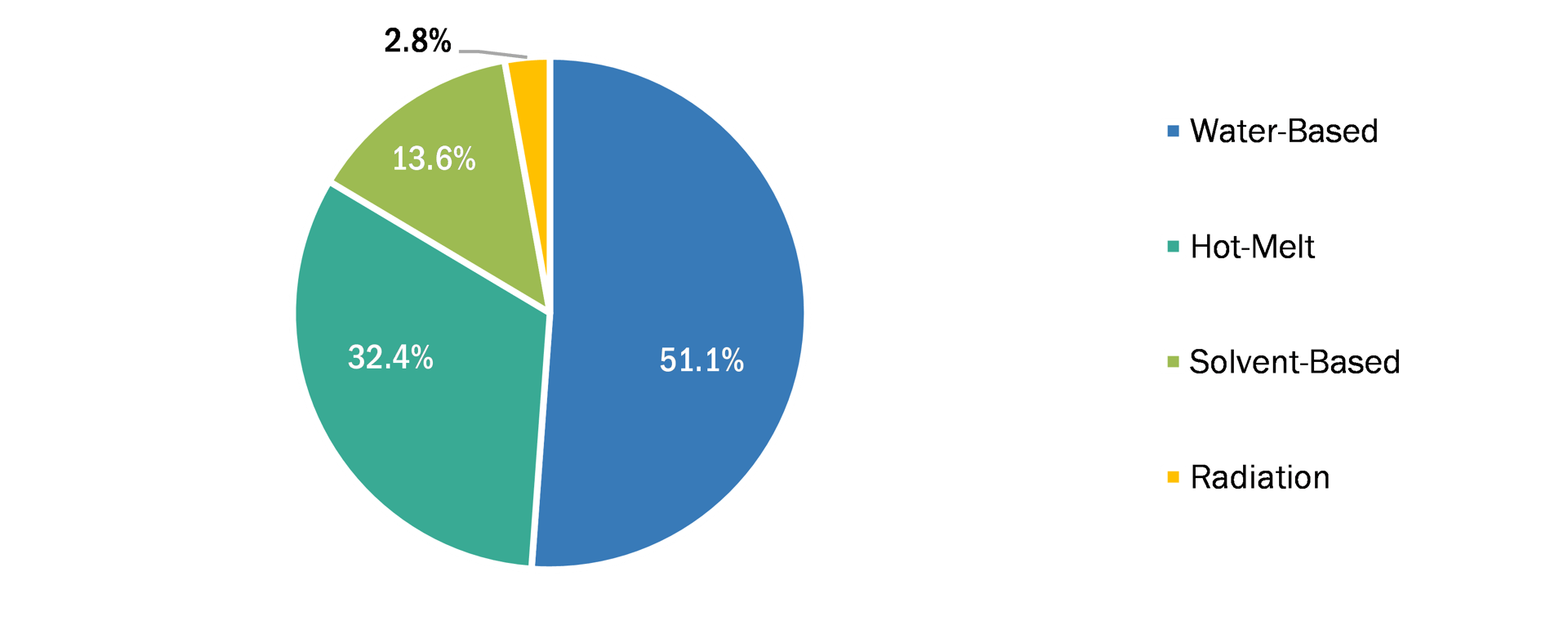

Figure 3: Water-based was the dominant technology in the PSA market in 2025. Source: secondary research, interviews with experts, and MarketsandMarkets analysis.

Stringent Environmental Regulations to Drive the Demand for Water-based Technology

Water-based PSAs have emerged as the leading technology, fueled by the increasing demand for environmentally responsible, low-VOC adhesive solutions. These systems offer a compelling combination of performance, sustainability, and regulatory compliance, making them the preferred choice across high-volume applications such as packaging, tapes, labels, and hygiene products. Their ease of formulation, compatibility with a variety of polymers (primarily acrylics), and ability to deliver consistent tack, peel, and shear strength further reinforce their dominance.

The growing stringency of environmental regulations worldwide, particularly restrictions on VOCs in North America, Europe, and Asia-Pacific, has accelerated the adoption of water-based systems. Unlike traditional solvent-based PSAs, water-based adhesives significantly reduce VOC emissions, aligning with corporate sustainability goals and eco-labeling requirements for packaging and consumer products. In terms of applications, water-based PSAs are widely used in food and beverage labeling, flexible packaging, protective films, and masking tapes, where both performance and regulatory compliance are critical. The technology's adaptability also extends to hygiene products and medical devices, including disposable wound dressings and transdermal patches, where skin-friendly, low-migration adhesives are essential.

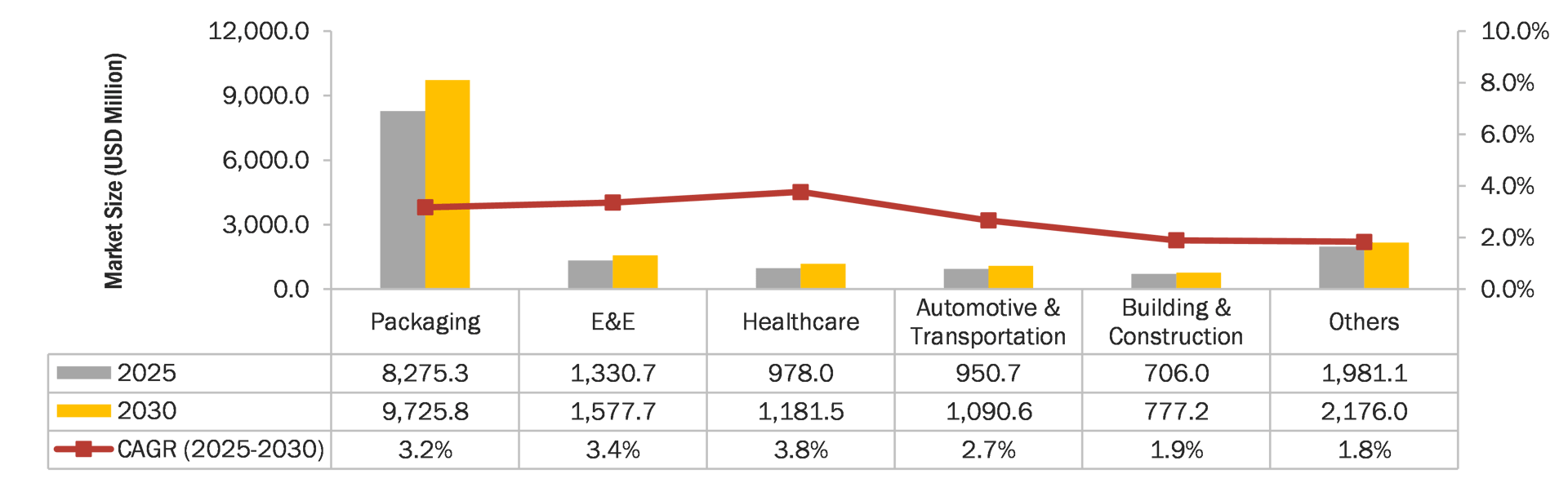

Figure 4: Packaging to lead PSA demand between 2025 and 2030. Note: E&E include electrical and electronics and telecommunications. Source: secondary research, interviews with experts, and MarketsandMarkets analysis.

High-Volume Packaging Applications Anchor PSA Market Leadership

The packaging industry remains the largest end-use segment for PSAs. Several converging trends in packaging are driving PSAs growth and shaping market dynamics. The rapid expansion of e-commerce and the surge in online retail have created unprecedented demand for packaging tapes, labels, and protective films capable of withstanding high-speed automated processing and transit stresses. PSAs, particularly acrylic and water-based systems, are ideally suited to meet these requirements, offering strong adhesion, durability, and adaptability to a wide variety of substrates, including paper, plastics, and flexible films.

Sustainability and regulatory pressures are also influencing PSAs adoption in packaging. Growing consumer awareness of environmental impact combined with stricter global regulations on VOC emissions and recyclability are fueling the shift toward water-based and bio-based adhesive technologies. Moreover, packaging innovation such as flexible and lightweight materials, smart labels, and tamper-evident seals is further driving PSAs usage. These high-performance applications require adhesives that maintain strong bonding under variable temperatures, humidity, and mechanical stress, while remaining easy to convert in high-speed production lines.

Industry Leaders and Evolving Strategies

The key manufacturers of PSAs are Henkel AG, Dow Inc., H.B. Fuller Co., 3M Co., Avery Dennison Corp., Arkema SA, Sika AG, Scapa Group plc., Wacker Chemie AG, and Illinois Tool Works, Inc. (ITW). These players are actively present in the market and undertook strategic initiatives such as new product launches, mergers and acquisitions, partnership and agreements, and expansions etc.

In February2026, Henkel announced a strategic collaboration with SEKAB to accelerate the transition from fossil‑based solvents (such as ethyl acetate) to bio-based raw materials in adhesive production. While this is a partnership rather than a product launch, it is directly tied to next‑generation PSA formulation technology aimed at sustainability without sacrificing performance.

In September2025, BioBond announced the launch of its BioMelt Pressure Sensitive Adhesive product offerings, a plant‑based PSA portfolio designed for labels, tape, and various industrial and consumer markets. These bio-based solutions are USDA BioPreferred‑certified, PFAS‑free, with no microplastics or odors.

Future Market Trends

Looking ahead, several trends are poised to shape the future of PSAs. They include the following.

Bio-based and Circular PSAs: As sustainability becomes a central industry imperative, PSA formulations are shifting toward bio-based raw materials and circular design principles. These next‑generation PSAs use renewable feedstocks, reduce reliance on petrochemicals, and are engineered for recyclability or compostability. The result is adhesives that maintain performance while enabling recyclable packaging streams and reducing environmental footprint.

High-Performance PSAs for Next-Gen Electronics: PSAs are becoming central to advanced electronics design, including flexible displays, wearables, and miniaturized components. Future PSA systems will prioritize ultra‑thin, heat‑resistant, and transparent formulations that can withstand high operating temperatures and rigorous performance demands. Integration with advanced substrates and conductive materials is driving this trend.

Low-Migration PSAs for Sensitive Applications: With expanding regulations governing skin contact, food packaging, and medical use, there is a strong push toward low‑migration, non‑toxic PSA formulations. These adhesives minimize extractables and ensure safety compliance, especially in direct food contact labels, wearable medical patches, and hygiene products. The focus is on balancing adhesion performance with regulatory demands.

Next-Generation Recycling-Friendly Adhesives: One of the biggest challenges in packaging recyclability is adhesive residue interfering with fiber recovery or film streams. Future PSA technologies are being engineered to detach cleanly during recycling processes, enabling higher quality secondary materials. Wash‑off, repulpable, and thermally removable PSAs will become mainstream to support circular packaging ecosystems.

Microstructure Engineered PSAs for Precision Bonding: Advances in polymer science and processing are allowing manufacturers to design PSA microstructures that deliver optimized performance in specific use cases. Tailored viscoelastic profiles, controlled fibrillar networks, and nano‑scale crosslinking strategies help create PSAs with precise tack, peel, and shear balance, enhancing consistency and reliability in demanding automated manufacturing.

Digital Formulation and AI Driven PSAs Development: The use of computational modelling and artificial intelligence is accelerating PSA innovation cycles. By simulating polymer interactions and performance outcomes, developers can predict optimal formulations, shorten R&D timelines, and tailor adhesives to unique customer needs. This trend will lead to faster, more efficient, and highly customized PSA solutions.

Conclusion

The PSAs market is poised for sustained growth, driven by increasing demand across packaging, electronics, automotive, and healthcare sectors. Acrylic-based chemistries and water-based technologies continue to dominate, offering a balance of performance, sustainability, and regulatory compliance. Leading players are focusing on formulation innovations, sustainability-driven product development, and strategic collaborations to address evolving end-use requirements. Recent developments highlight advancements in bio-based, compostable, and low-VOC PSA formulations, while future trends point toward smart, responsive adhesives, recycling-friendly solutions, and AI-enabled custom formulations. The Asia-Pacific region remains a major growth hub due to rapid industrialization, rising packaging demand, and technological adoption. As the industry increasingly integrates multifunctional materials, high-performance polymers, and environmentally conscious chemistries, PSA solutions are evolving beyond simple bonding agents to critical enablers of performance, sustainability, and innovation across diverse applications.

Learn more about market research from MarketsandMarkets by visiting www.marketsandmarkets.com.

Opening image courtesy of Memedozaslan / iStock / Getty Images Plus.